How much car dealers make, how to get thousands back

- Jeff Guymon

- Apr 19, 2020

- 5 min read

Updated: Aug 13, 2020

Before the world turned digital, purchasing a vehicle was done entirely in person. Newspaper advertisements and classified pages were the go-to places to find details about used cars. To learn more about cars, shoppers had to visit and spend hours at car dealerships.

Table of contents

Dealers used to have high margins

Along comes the Internet, consumers can compare car prices

So how do dealers make their money?

How to refinance your auto loan and save thousands of dollars

Dealers used to have high margins

However, a lack of transparency meant the only way to find a fair price for a vehicle involved traveling hundreds of miles. Customers visited many different dealerships over multiple weekends, effectively allowing dealers to set their own prices.

Setting their own prices meant high profit margins and in some instances, dealerships could be making up to 15% and more on each vehicle and make another $1,500 - $3,000 on a trade-in. For example, on a sticker price of $25,000 used car dealers often made $3,750 in profit while car buyers were in the dark.

In addition to the profits on each vehicle, dealerships were also the primary source of securing financing, add-ons and protection plans (such as GAP insurance, extended warranties, vehicle service contracts, maintenance plans etc.). These products typically feature even higher margins:

On an extended warranty of $2,000, the dealer makes up to $1,000 in profit.

On a $700 GAP insurance policy, the dealer usually makes up to $550 in profit.

Along comes the Internet, consumers can compare car prices

Before the start of the new millennium, car dealerships were enjoying big profits. However, as the world became more digital, car sales went online: Craigslist replaced offline classifieds and Autotrader.com, Cars.com and Cargurus.com launched to replace newspaper ads for used vehicles.

The Internet transformed the way consumers shop for new vehicles, finance and insurance. Long gone are the days of visiting multiple dealerships to compare MSRPs and find the best price of the cars. Nowadays, car shoppers conduct 59% of their research online and an average customer looks at 11 different websites before visiting an auto dealership.

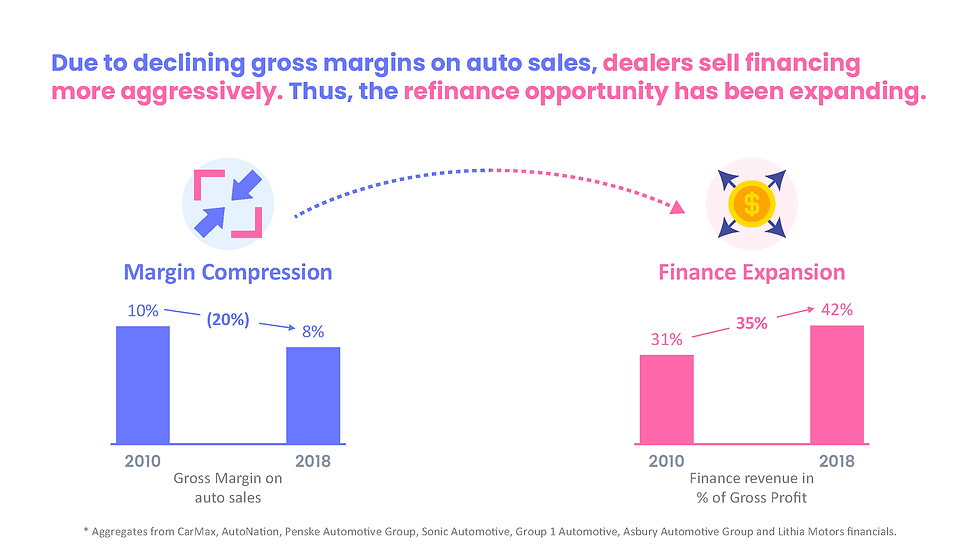

The Internet offered an increased level of transparency. New car and used car price reference pages showed up (e.g. Nada, Edmunds, KBB) and educating consumers about what a vehicle should cost before ever talking to a salesman. As a result, dealers had to give up margin to remain competitive. The bottom line: margins and gross profit on cars dropped by 20% over the last 10 years.

So how do dealers make their money?

To combat declining profits, dealers have started focusing on the more opaque, high-margin finance and protection products, which drastically changed how car dealers make money. While losing 20% of profit on the actual vehicles, dealers made up for the loss by generating 35% more profit on financing.

Today, dealers focus heavily on what they call back-end products:

The commission paid car salesperson and the financing managers in the dealership now more than ever convince customers to finance their car purchase and minimize their down payments - even if the customer has the necessary cash!

When offering financing, dealers mark up interest rates on each loan, ensuring they receive even more profit. I.e. without car shoppers knowing, the dealership raises the interest rate on a loan to make additional profit. The F&I department has become a significant profit center.

Lastly, dealers have become very savvy in selling protection products such as extended warranties, GAP insurance and other plans with very high margins – many of which have little to no value to the customer.

Unlike other major purchases we make in life - e.g. such as purchasing a home - cars are in reality very impulsive purchases. Everything during the car buying process and in the showroom - including your financing application - happens quickly the second you set foot on a dealership lot. Dealers have become very sharp sales people and good negotiators. Customers therefore rarely get the chance to compare loan terms once they test drove and fell in love with a car.

Instead, the sales personnel at the dealership tends to pressure customers into taking the dealer’s finance offer, often using arguments such as ‘... this offer is only valid today!’.

As a result, 79% of consumers get their financing from the dealer and at suboptimal terms and loan rates. For customers with exceptionally good credit, getting financing at the dealership is not an issue. When you have perfect credit, you know that you qualify for the lowest possible interest rate at 2% or below. Most American, however, don’t have perfect credit.

The loan rates for credit scores below 700, however, are all over the map. We recently performed a study 'Lower your rate now. The car loan market is inefficient' and found that likely up to 50% of Americans overpay up to $37 billion in interest on their auto loans every single year.

Once you fell in love with your next car, dealers have an easy time avoiding the ‘... what’s the interest rate on my loan?' conversation and instead shift the focus on monthly payments. Any interest rate mark-up goes straight into the dealer’s pocket. The dealer can easily disguise the higher loan rates by stretching the loan over a few more months and focus his conversation on monthly payments.

We took a look at the financial statements of the top 10 publicly listed dealership groups and found that all of them make more money on financing and protection plans (i.e. the F&U profit center) than on the actual cars they are selling. This effect is even more pronounced on new car sales, also because of the dealer incentives and rebates typical for new cars.

Some dealership groups make on average north of $2,300 on these opaque and hard to understand financing and protection products:

How to refinance your auto loan and save thousands of dollars

When we performed our study above, we felt frustrated for a lot of car owners. More than likely, a lot of hard-working Americans have purchased protection products, GAP insurance and extended warranties they aren't using and have been overpaying on interest and monthly payments.

Thankfully, we can help you with two things here:

Understand and cancel protection products: Vehicle Service contract, Prepaid Maintenance contract, Ding & Dent protection, GAP waiver ... lost track of what the dealer sold you? We'll help you understand your protection products and cancel the ones you don't need.

Lower your monthly payments: In our article 'The best way to lower your rate? Make your payments!' we found that a lot of Americans can refinance their car loans and save thousands of dollars.

WithClutch.com is a fully digital platform that lets car owners like you do so from the comfort of their own home. No need to set a foot in a bank or credit union. You can lower your rate or get cash in as little as 20 seconds.

Follow three simple steps to refinance your auto loan, get approved in seconds and save thousands in minutes.

Comments